90. The Aiyagari Model with Endogenous Grid Method#

In addition to what’s included in base Anaconda, we need to install QuantEcon’s Python library and JAX.

!pip install quantecon jax

90.1. Overview#

This lecture combines two important computational methods in macroeconomics:

The Aiyagari model [Aiyagari, 1994] – a heterogeneous agent model with incomplete markets

The endogenous grid method (EGM) [Carroll, 2006] – an efficient algorithm for solving dynamic programming problems

In the standard Aiyagari lecture, we solved the household problem using discretization and value function iteration.

We then computed aggregate capital at a given set of prices using the stationary distribution of the finite Markov chain.

In this lecture, we take a different approach:

We use the endogenous grid method to solve the household problem via the Euler equation and linear interpolation.

We compute aggregate capital by simulation rather than an algebraic technique (which only works for the finite case).

These modifications make the solution method faster and more flexible, especially when dealing with more complex models.

We use JAX throughout, so that the EGM operator, the solver and the simulation are all JIT-compiled and vectorized.

90.1.1. References#

The primary references for this lecture are:

our previous Aiyagari lecture for the key ideas

[Aiyagari, 1994] for the economic model

[Carroll, 2006] for the endogenous grid method

Chapter 18 of [Ljungqvist and Sargent, 2018] for textbook treatment

90.1.2. Preliminaries#

We use the following imports:

import quantecon as qe

import matplotlib.pyplot as plt

import jax

import jax.numpy as jnp

import numpy as np

from typing import NamedTuple

from functools import partial

from scipy.optimize import bisect

We will use 64-bit floats with JAX in order to increase precision.

jax.config.update("jax_enable_x64", True)

90.2. The Economy#

The economy consists of households and a representative firm.

90.2.1. Households#

Infinitely lived households face idiosyncratic income shocks and a borrowing constraint.

The savings problem faced by a typical household is

subject to

where

\(c_t\) is current consumption

\(a_t\) is assets

\(z_t\) is an exogenous component of labor income (stochastic employment status)

\(w\) is the wage rate

\(r\) is the interest rate

\(B\) is the maximum amount that the agent is allowed to borrow

The exogenous process \(\{z_t\}\) follows a finite state Markov chain with stochastic matrix \(\Pi\).

Optimal interior consumption choices satisfy the Euler equation

(We use \('\) symbols for both derivatives and future values, which is not ideal but convenient and common.)

In terms of assets, this is

where \(s\) is the optimal savings policy function.

90.2.2. Firms#

Firms produce output by hiring capital and labor under constant returns to scale.

The representative firm’s output is

where

\(A\) and \(\alpha\) are parameters with \(A > 0\) and \(\alpha \in (0, 1)\)

\(K\) is aggregate capital

\(N\) is total labor supply (normalized to 1)

These parameters are stored in the following namedtuple:

class Firm(NamedTuple):

A: float = 1.0 # Total factor productivity

N: float = 1.0 # Total labor supply

α: float = 0.33 # Capital share

δ: float = 0.05 # Depreciation rate

From the firm’s first-order condition, the inverse demand for capital is

def r_given_k(K, firm):

"""

Inverse demand curve for capital.

"""

A, N, α, δ = firm

return A * α * (N / K)**(1 - α) - δ

The equilibrium wage rate as a function of \(r\) is

def r_to_w(r, firm):

"""

Equilibrium wages associated with a given interest rate r.

"""

A, N, α, δ = firm

return A * (1 - α) * (A * α / (r + δ))**(α / (1 - α))

90.2.3. Equilibrium#

A stationary rational expectations equilibrium (SREE) consists of prices and policies such that:

Households optimize given prices

Firms maximize profits given prices

Markets clear: aggregate capital supply equals aggregate capital demand

Aggregate quantities are constant over time

90.3. Implementation with EGM#

90.3.1. Household primitives#

First we set up the household parameters and grids:

class Household(NamedTuple):

β: float # Discount factor

a_grid: jnp.ndarray # Asset grid

z_grid: jnp.ndarray # Exogenous states

Π: jnp.ndarray # Transition matrix

def create_household(β=0.96, # Discount factor

Π=[[0.9, 0.1], [0.1, 0.9]], # Markov chain

z_grid=[0.1, 1.0], # Exogenous states

a_min=1e-10, a_max=50.0, # Asset grid

a_size=200):

"""

Create a Household namedtuple with custom grids.

"""

a_grid = jnp.linspace(a_min, a_max, a_size)

z_grid, Π = map(jnp.array, (z_grid, Π))

return Household(β=β, a_grid=a_grid, z_grid=z_grid, Π=Π)

For utility, we assume \(u(c) = \log(c)\), which gives us \(u'(c) = 1/c\) and \((u')^{-1}(x) = 1/x\).

@jax.jit

def u_prime(c):

return 1 / c

@jax.jit

def u_prime_inv(x):

return 1 / x

Here’s a namedtuple for prices:

class Prices(NamedTuple):

r: float = 0.01 # Interest rate

w: float = 1.0 # Wages

90.3.2. The EGM operator#

The key insight of EGM is to avoid root-finding by choosing the asset grid exogenously and computing the consumption values directly from the Euler equation.

The Coleman-Reffett operator using EGM works as follows:

Start with a consumption policy \(\sigma\) represented on an exogenous grid of (next-period) assets \(\{a_i\}\).

For each asset level \(a_i\) and current employment state \(z_j\):

Compute the right-hand side of the Euler equation: $\(\text{RHS} = \beta (1 + r) \sum_{z'} \Pi(z_j, z') \, u'(\sigma(a_i, z'))\)$

Use the inverse marginal utility to get current consumption: $\(c_{ij} = (u')^{-1}(\text{RHS})\)$

Recover the implied current asset level from the budget constraint: $\(a_{ij} = \frac{c_{ij} + a_i - w z_j}{1 + r}\)$

Reconstruct the new policy \(K\sigma\) on the original asset grid by interpolating \((a_{ij}, c_{ij})\), handling the borrowing constraint where it binds.

The whole operation vectorizes cleanly, so we write it as a single JIT-compiled function and use vmap over the employment states:

@jax.jit

def K_egm(σ, household, prices):

"""

The Coleman-Reffett operator using EGM for the Aiyagari model.

Here σ[i, j] is consumption when next-period assets are a_grid[i]

and the current employment state is z_grid[j].

"""

β, a_grid, z_grid, Π = household

r, w = prices

z_size = len(z_grid)

# Expectation E[u'(c(a', z')) | z] over the next-period shock

Eu_prime = (Π @ u_prime(σ).T).T # (a_size, z_size)

# Euler equation -> consumption on the endogenous grid

c_endo = u_prime_inv(β * (1 + r) * Eu_prime) # (a_size, z_size)

# Implied current assets: a = (c + a' - w z) / (1 + r)

a_endo = (c_endo + a_grid[:, None] - w * z_grid[None, :]) / (1 + r)

# Interpolate back onto the exogenous grid for each employment state

def interp_policy(j):

# Where today's assets fall below the endogenous grid the borrowing

# constraint binds, so the household saves a_grid[0] and consumes

# the rest of current income.

return jnp.where(

a_grid < a_endo[0, j],

w * z_grid[j] + (1 + r) * a_grid - a_grid[0],

jnp.interp(a_grid, a_endo[:, j], c_endo[:, j])

)

σ_new = jax.vmap(interp_policy)(jnp.arange(z_size)) # (z_size, a_size)

return σ_new.T # (a_size, z_size)

90.3.3. Solving the household problem#

We solve for the optimal policy by iterating the EGM operator to convergence.

The solver is fully JIT-compiled and uses jax.lax.while_loop for the iteration:

@jax.jit

def solve_household(household, prices, tol=1e-6, max_iter=10_000):

"""

Solve the household problem by iterating the EGM operator.

Returns the optimal consumption policy σ[i, j], where i indexes

next-period assets and j indexes employment states.

"""

β, a_grid, z_grid, Π = household

r, w = prices

# Initial guess: consume half of current income

income = w * z_grid[None, :] + (1 + r) * a_grid[:, None]

σ_init = 0.5 * income

def condition(state):

i, σ, error = state

return (error > tol) & (i < max_iter)

def body(state):

i, σ, error = state

σ_new = K_egm(σ, household, prices)

error = jnp.max(jnp.abs(σ_new - σ))

return i + 1, σ_new, error

i, σ, error = jax.lax.while_loop(condition, body, (0, σ_init, tol + 1))

return σ

Let’s test this on an example:

household = create_household()

prices = Prices(r=0.01, w=1.0)

with qe.Timer():

σ_star = solve_household(household, prices)

jax.block_until_ready(σ_star)

0.3651 seconds elapsed

We can check that the policy is a fixed point of the EGM operator by measuring the residual:

residual = jnp.max(jnp.abs(K_egm(σ_star, household, prices) - σ_star))

print(f"Final Euler residual: {residual:.2e}")

Final Euler residual: 8.34e-07

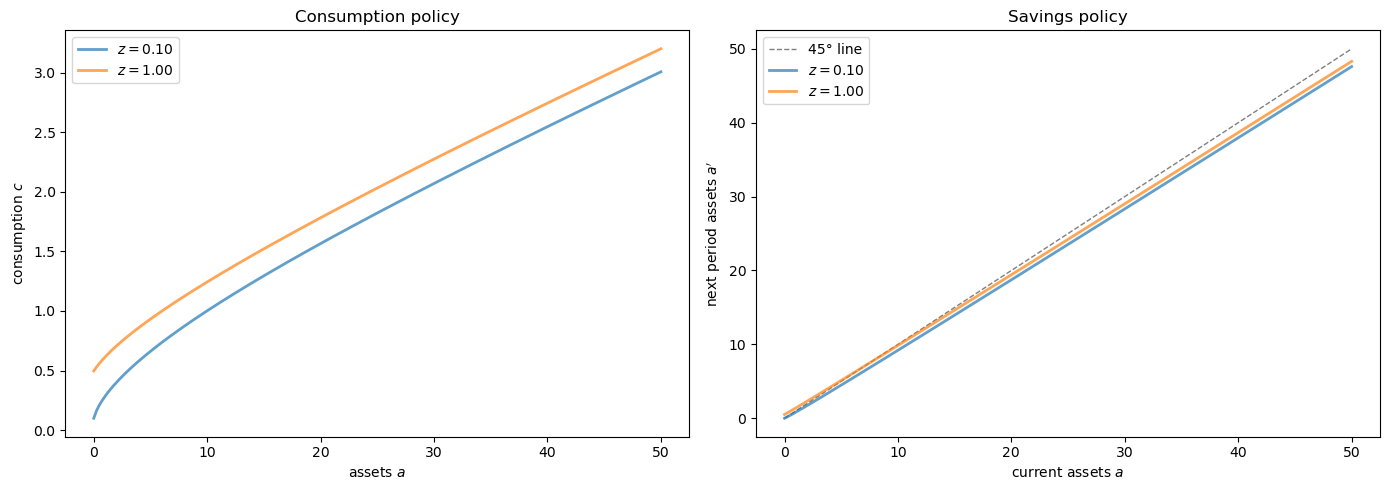

Let’s plot the resulting policy functions:

β, a_grid, z_grid, Π = household

r, w = prices

# Convert consumption policy to savings policy

income = w * z_grid[None, :] + (1 + r) * a_grid[:, None]

savings = income - σ_star

fig, axes = plt.subplots(1, 2, figsize=(14, 5))

# Plot consumption policy

ax = axes[0]

for j, z in enumerate(z_grid):

ax.plot(a_grid, σ_star[:, j], label=f'$z={z:.2f}$', lw=2, alpha=0.7)

ax.set_xlabel('assets $a$')

ax.set_ylabel('consumption $c$')

ax.set_title('Consumption policy')

ax.legend()

# Plot savings policy

ax = axes[1]

ax.plot(a_grid, a_grid, 'k--', lw=1, alpha=0.5, label='45° line')

for j, z in enumerate(z_grid):

ax.plot(a_grid, savings[:, j], label=f'$z={z:.2f}$', lw=2, alpha=0.7)

ax.set_xlabel('current assets $a$')

ax.set_ylabel("next period assets $a'$")

ax.set_title('Savings policy')

ax.legend()

plt.tight_layout()

plt.show()

90.4. Computing Aggregate Capital by Simulation#

Instead of computing the stationary distribution of the Markov chain analytically, we compute aggregate capital by simulating a large cross-section of households.

This approach:

is more flexible (works with continuous shocks, non-linear policies, etc.)

avoids storing and manipulating large transition matrices

is conceptually simpler

The simulation is fully vectorized: we advance all households simultaneously with jax.lax.fori_loop, drawing the employment transitions by inverse-CDF sampling and looking up consumption with a vmap-ed interpolation.

@partial(jax.jit, static_argnames=('num_households', 'num_periods'))

def simulate_cross_section(σ, household, prices, key,

num_households=50_000, num_periods=1_000):

"""

Simulate a panel of households forward and return the terminal

cross-section of assets and employment states.

"""

β, a_grid, z_grid, Π = household

r, w = prices

# CDF of each row of Π, used for inverse-CDF sampling of transitions

Π_cdf = jnp.cumsum(Π, axis=1)

# Vectorized consumption lookup: interpolate σ along assets for each z

@jax.vmap

def consume(a, j):

return jnp.interp(a, a_grid, σ[:, j])

# Initial conditions: everyone at the middle of the grid, in state 0

assets = jnp.full(num_households, a_grid[len(a_grid) // 2])

z_idx = jnp.zeros(num_households, dtype=jnp.int32)

def step(t, state):

assets, z_idx, key = state

key, subkey = jax.random.split(key)

unif = jax.random.uniform(subkey, (num_households,))

# Markov transition via inverse CDF

z_idx = (unif[:, None] > Π_cdf[z_idx]).sum(axis=1).astype(jnp.int32)

# Budget constraint: consume, then carry assets to next period

income = w * z_grid[z_idx] + (1 + r) * assets

assets = income - consume(assets, z_idx)

# Enforce the asset grid bounds

assets = jnp.clip(assets, a_grid[0], a_grid[-1])

return assets, z_idx, key

assets, z_idx, key = jax.lax.fori_loop(

0, num_periods, step, (assets, z_idx, key)

)

return assets, z_idx

Now we can compute capital supply for given prices by solving the household problem and averaging assets across the simulated cross-section:

def capital_supply(household, prices, key,

num_households=50_000, num_periods=1_000):

"""

Compute aggregate capital supply by simulation.

"""

σ = solve_household(household, prices)

assets, _ = simulate_cross_section(

σ, household, prices, key,

num_households=num_households, num_periods=num_periods

)

return float(jnp.mean(assets))

Let’s test it:

household = create_household()

prices = Prices(r=0.01, w=1.0)

key = jax.random.PRNGKey(42)

with qe.Timer():

K_supply = capital_supply(household, prices, key)

print(f"Capital supply: {K_supply:.4f}")

0.9121 seconds elapsed

Capital supply: 2.5863

90.5. Computing Equilibrium#

Now we can compute the equilibrium by finding the capital stock at which capital supply equals capital demand.

Given \(K\), the equilibrium mapping \(G\) computes:

prices \((r, w)\) from the firm’s first-order conditions,

the household’s optimal policy given those prices,

aggregate capital supply via simulation.

def G(K, firm, household, key,

num_households=50_000, num_periods=1_000):

"""

The equilibrium mapping K -> capital supply.

"""

r = r_given_k(K, firm)

w = r_to_w(r, firm)

prices = Prices(r=r, w=w)

return capital_supply(household, prices, key,

num_households=num_households,

num_periods=num_periods)

We compute the equilibrium by applying bisection to the excess demand \(K - G(K)\).

We pass a fixed random key to every evaluation so that the excess demand function is deterministic, as required by the root finder.

def compute_equilibrium(firm, household, key,

K_min=4.0, K_max=12.0,

num_households=50_000, num_periods=1_000,

xtol=1e-2):

"""

Compute the equilibrium capital stock using bisection.

"""

def excess_demand(K):

return K - G(K, firm, household, key,

num_households=num_households,

num_periods=num_periods)

return bisect(excess_demand, K_min, K_max, xtol=xtol)

Let’s compute the equilibrium:

firm = Firm()

household = create_household()

key = jax.random.PRNGKey(42)

with qe.Timer():

K_star = compute_equilibrium(firm, household, key)

r_star = r_given_k(K_star, firm)

w_star = r_to_w(r_star, firm)

print(f"\nEquilibrium capital: {K_star:.4f}")

print(f"Equilibrium interest rate: {r_star:.4f}")

print(f"Equilibrium wage: {w_star:.4f}")

1.8785 seconds elapsed

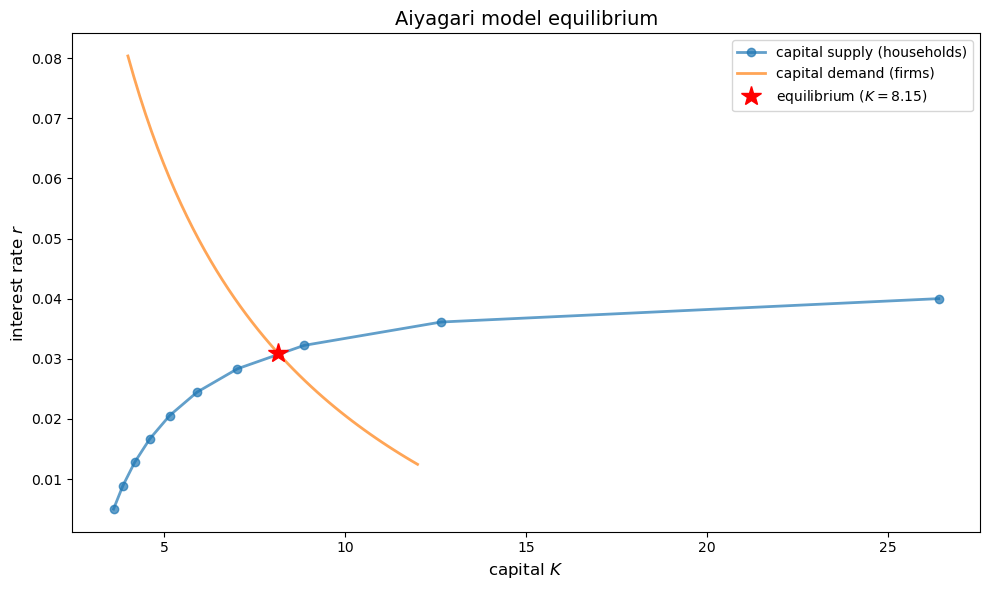

Equilibrium capital: 8.1484

Equilibrium interest rate: 0.0309

Equilibrium wage: 1.3388

90.5.1. Visualizing equilibrium#

Let’s plot the supply and demand curves:

# Supply curve: capital supplied by households as a function of r

r_vals = np.linspace(0.005, 0.04, 10)

K_supply_vals = []

for r in r_vals:

w = r_to_w(r, firm)

prices = Prices(r=r, w=w)

K_supply_vals.append(capital_supply(household, prices, key))

# Demand curve: capital demanded by firms as a function of r

K_vals = np.linspace(4, 12, 50)

r_demand_vals = r_given_k(K_vals, firm)

fig, ax = plt.subplots(figsize=(10, 6))

ax.plot(K_supply_vals, r_vals, 'o-', lw=2, alpha=0.7,

label='capital supply (households)', markersize=6)

ax.plot(K_vals, r_demand_vals, lw=2, alpha=0.7,

label='capital demand (firms)')

ax.plot(K_star, r_star, 'r*', markersize=15, zorder=5,

label=f'equilibrium ($K={K_star:.2f}$)')

ax.set_xlabel('capital $K$', fontsize=12)

ax.set_ylabel('interest rate $r$', fontsize=12)

ax.set_title('Aiyagari model equilibrium', fontsize=14)

ax.legend(fontsize=10)

plt.tight_layout()

plt.show()

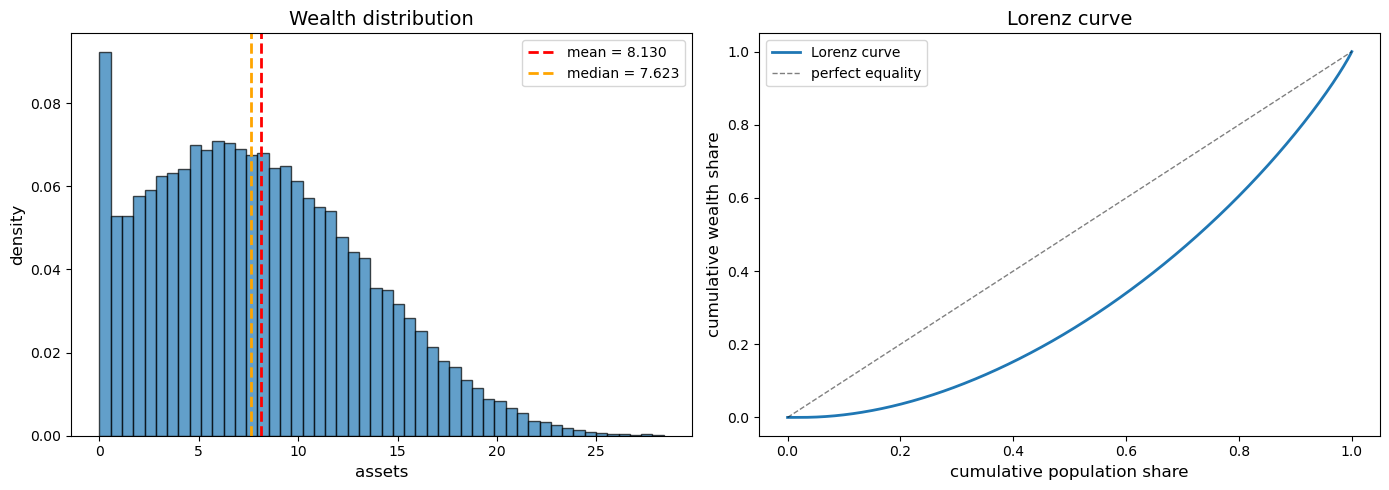

90.6. Wealth Distribution#

One advantage of the simulation approach is that we can easily examine the wealth distribution.

We reuse the cross-section simulated at equilibrium prices:

prices_star = Prices(r=r_star, w=w_star)

σ_star = solve_household(household, prices_star)

assets_dist, z_dist = simulate_cross_section(σ_star, household, prices_star, key)

assets_dist = np.asarray(assets_dist)

We use QuantEcon’s lorenz_curve and gini_coefficient to summarize inequality:

fig, axes = plt.subplots(1, 2, figsize=(14, 5))

# Histogram

ax = axes[0]

ax.hist(assets_dist, bins=50, density=True, alpha=0.7, edgecolor='black')

ax.axvline(np.mean(assets_dist), color='red', linestyle='--', linewidth=2,

label=f'mean = {np.mean(assets_dist):.3f}')

ax.axvline(np.median(assets_dist), color='orange', linestyle='--', linewidth=2,

label=f'median = {np.median(assets_dist):.3f}')

ax.set_xlabel('assets', fontsize=12)

ax.set_ylabel('density', fontsize=12)

ax.set_title('Wealth distribution', fontsize=14)

ax.legend()

# Lorenz curve

ax = axes[1]

cum_pop, cum_wealth = qe.lorenz_curve(assets_dist)

ax.plot(cum_pop, cum_wealth, lw=2, label='Lorenz curve')

ax.plot([0, 1], [0, 1], 'k--', lw=1, alpha=0.5, label='perfect equality')

ax.set_xlabel('cumulative population share', fontsize=12)

ax.set_ylabel('cumulative wealth share', fontsize=12)

ax.set_title('Lorenz curve', fontsize=14)

ax.legend()

plt.tight_layout()

plt.show()

gini = qe.gini_coefficient(assets_dist)

print(f"\nGini coefficient: {gini:.4f}")

Gini coefficient: 0.3645

90.7. Summary and Comparison#

This lecture demonstrated how to solve the Aiyagari model using:

Endogenous Grid Method (EGM) for the household problem

avoids costly root-finding by working backwards from the Euler equation

directly computes consumption from marginal utility

more efficient than value function iteration

Simulation for computing aggregate capital

simulates a large cross-section of households

more flexible than analytical stationary distributions

allows easy computation of wealth inequality measures

90.7.1. Comparison with standard approach#

Compared to the standard Aiyagari lecture:

Advantages:

EGM avoids the root-finding required by value function iteration

simulation is more flexible (works with continuous shocks, non-linear policies)

it is easy to compute distributional statistics (Gini, percentiles, etc.)

the approach is simpler to extend to more complex models

Disadvantages:

simulation requires a large number of households for accuracy

equilibrium computation is subject to Monte Carlo noise

it is less precise than the analytical stationary distribution

90.7.2. Extensions#

This framework can be easily extended to:

continuous income shocks (e.g., lognormal)

more complex preference specifications

aggregate shocks and heterogeneous agent New Keynesian (HANK) models

life-cycle models with age-dependent policies

90.8. Exercises#

Exercise 90.1

Compare the speed and accuracy of EGM against the value function iteration approach used in the standard Aiyagari lecture.

Solve the household problem with both methods at the same prices.

Time both methods and compare the resulting policies.

Which method is faster? Are the policies close?

Exercise 90.2

Study how the wealth distribution changes with the discount factor \(\beta\).

Compute equilibria for \(\beta \in \{0.94, 0.95, 0.96, 0.97\}\).

For each \(\beta\), compute and plot the wealth distribution.

How does the Gini coefficient change with \(\beta\)?

Explain the economic intuition.

Exercise 90.3

The simulation method introduced in this lecture uses a fixed number of periods. Investigate the impact of this choice:

Vary

num_periodsfrom 200 to 2000.For each value, compute the mean assets multiple times with different random keys.

Plot the standard deviation of the capital estimate as a function of

num_periods.What is the trade-off between accuracy and computational cost?

Exercise 90.4

Extend the model to include a third employment state (e.g., unemployed, part-time, full-time):

Set up a 3-state Markov chain with appropriate transition probabilities.

Define income levels for each state.

Re-compute the equilibrium.

How does the additional heterogeneity affect the wealth distribution?